Operating Thesis

Operating Thesis

Every major technology shift removes a barrier to skilled work. The same structural pattern follows every time.

Every major technology shift removes a barrier to entry for work that was previously expensive and skilled. The people doing that work face a decision: adapt to the new layer, or keep competing on the old one. The ones who adapt build what we call the verification layer — the craft of vouching for what the technology made cheap to produce. The Royal Society emerged to verify what came off the printing press. Reuters emerged to verify what came off the telegraph. The 1995 investment-banking analyst program was rebuilt around what Excel couldn't do — choosing the right model for the right question.

The economics are well-documented. Joel Spolsky described the mechanism in 2002: when one layer of a stack commoditizes, value migrates to the adjacent layer.1Clayton Christensen formalized it a year later as the Law of Conservation of Attractive Profits — when one stage becomes modular and commoditized, an adjacent stage becomes proprietary and captures the value.2Marc Andreessen's observation that software is "eating the world" was about the same structural force.3The pattern is older than any of these frameworks, but the frameworks make it predictable.

AI is the current layer shift. Analysis is the layer being commoditized.

A client with a Claude subscription has access to most of the analytical capability an advisor has. What they don't have is judgment under ambiguity, fiduciary accountability, or the ability to connect a recommendation to the qualitative reality of their own life. That's the verification layer. That's where the work moves. Everything below is what we believe follows from it, and what we're doing about it.

Section 1

The historical pattern

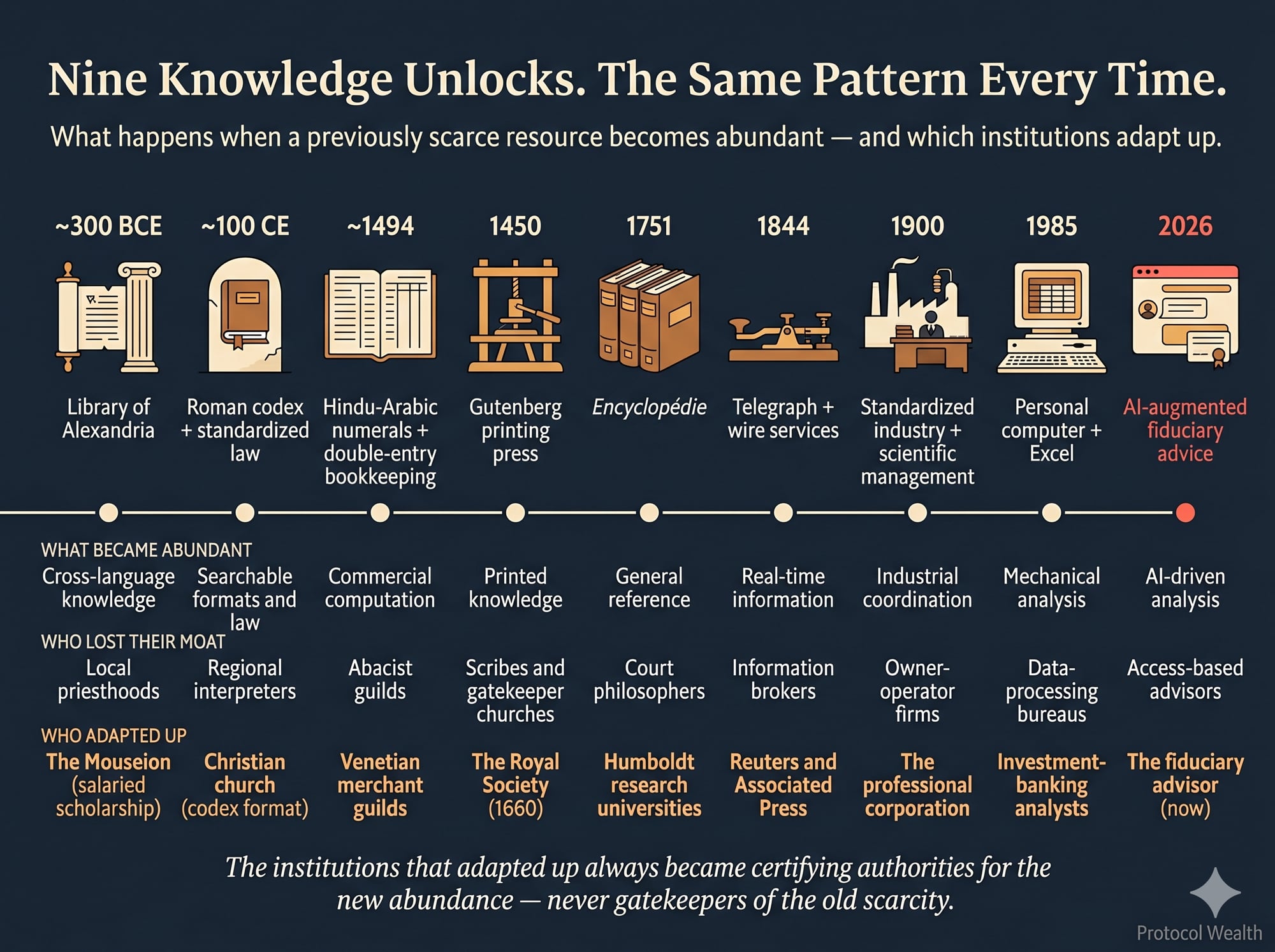

Over the past 2,300 years, technology has removed the barrier to skilled work nine distinct times. Each time the same thing happens. A new capability — the codex, the printing press, the telegraph, the spreadsheet — commoditizes a layer of work that was previously expensive. The people doing that work face a decision: adapt to the layer above, or keep competing on the one that just got cheap.

The list below is selective, not exhaustive. We chose nine moments where the layer shift is clearest. In every case, the work didn't disappear — it migrated upward. A new verification layer emerged on top of the disrupted one.

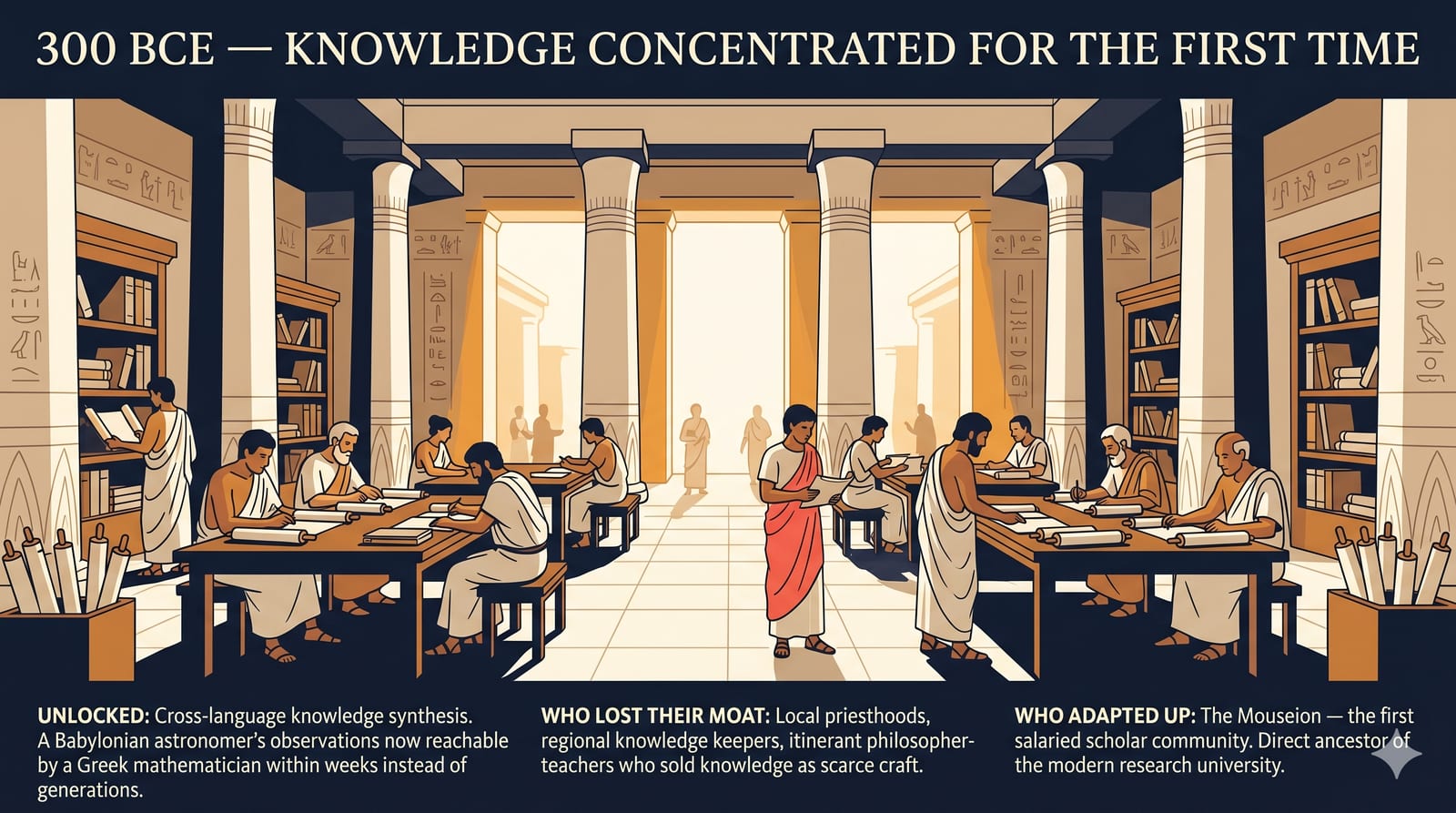

Panel 1 · ~300 BCE

Library of Alexandria

The first time humans concentrated knowledge from across cultures into a single searchable institution, they invented salaried scholarship. The modern research university descends directly from this moment.

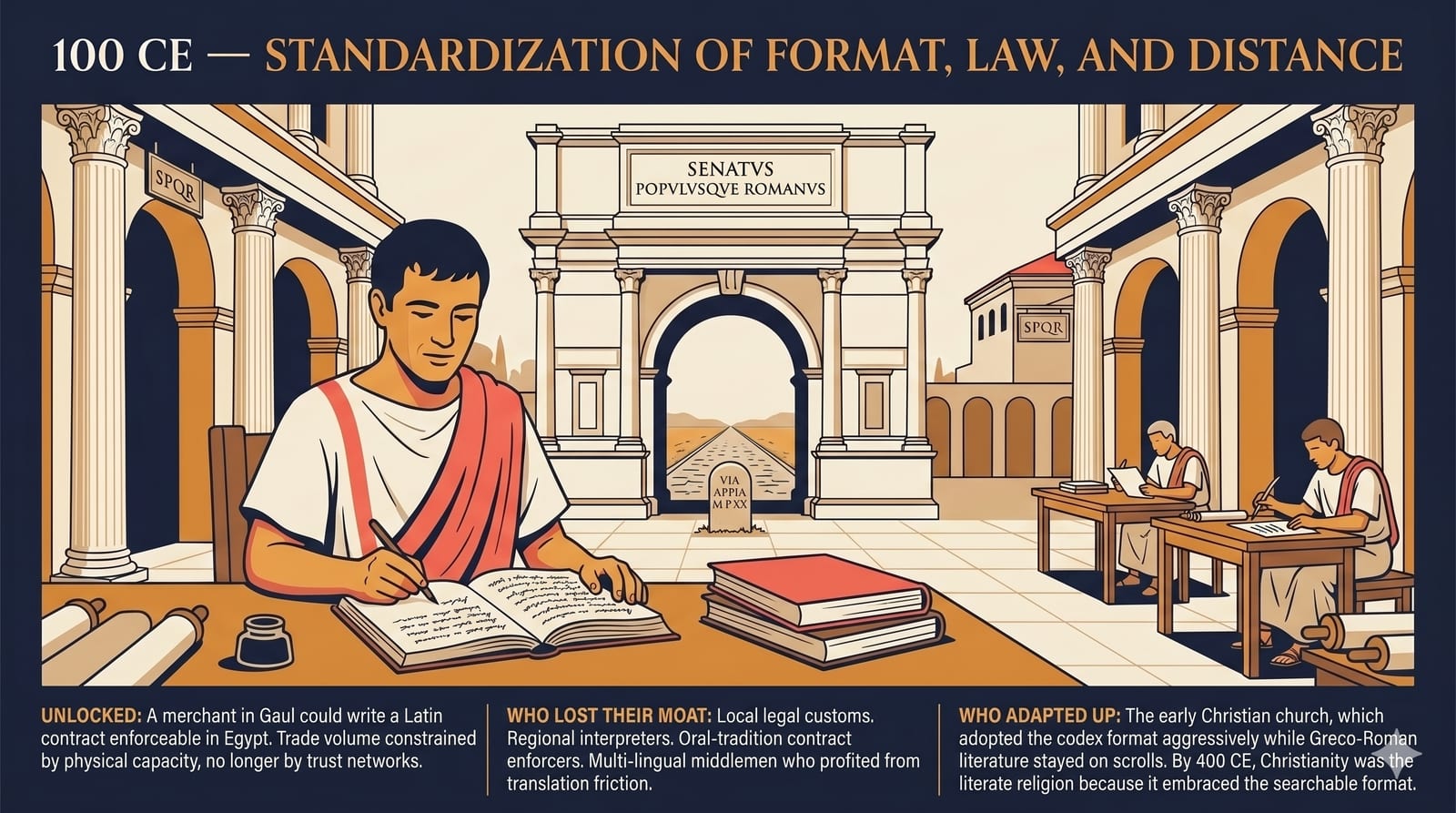

Panel 2 · ~100 CE

Roman codex and standardized law

Standardized format, standardized law, and standardized roads turned the Roman Empire into the first true cross-jurisdictional commercial system. The early Christian church embraced the new searchable book format aggressively while Greco-Roman literature stayed on scrolls. By 400 CE, Christianity was the literate religion because it embraced the better format.

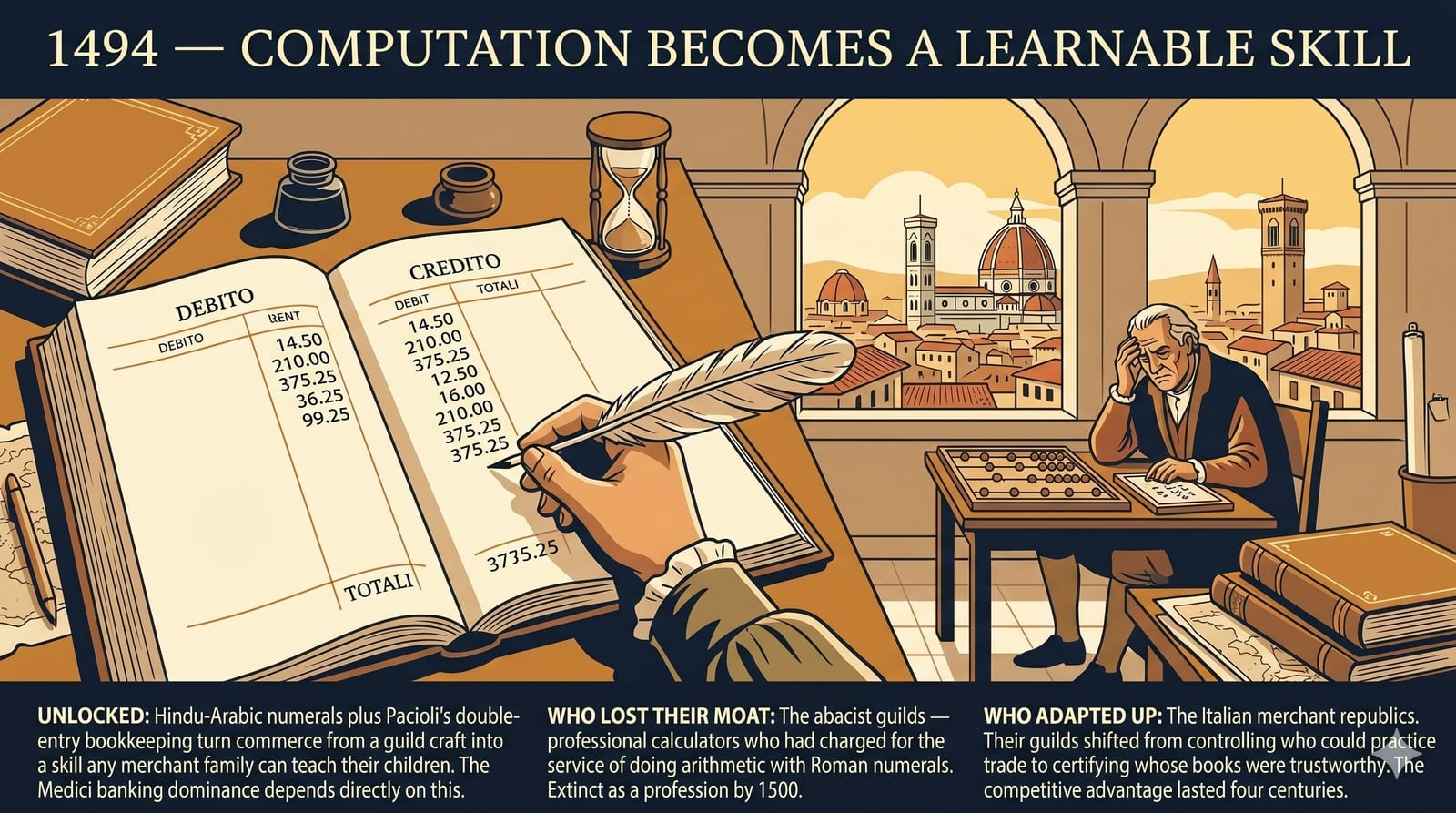

Panel 3 · 1494

Hindu-Arabic numerals and Pacioli

Hindu-Arabic numerals plus Luca Pacioli's double-entry bookkeeping turned commerce from a guild craft into a learnable skill. The abacist guilds — professional calculators who had charged for arithmetic with Roman numerals — went extinct as a profession by 1500. The Italian merchant republics' competitive advantage from this transition lasted four centuries.

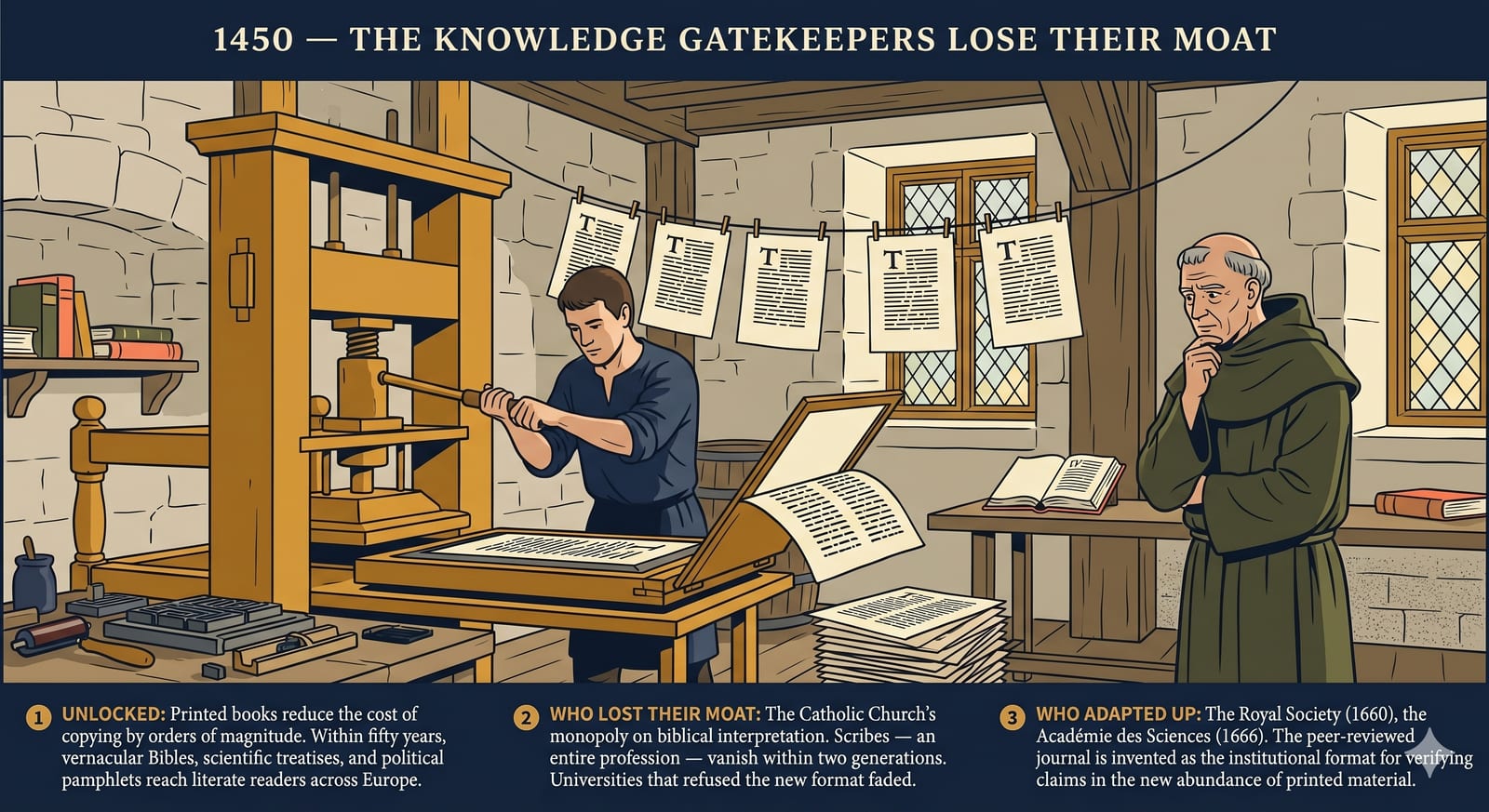

Panel 4 · 1450

Gutenberg printing press

Printed books reduced the cost of copying by orders of magnitude. The Catholic Church's monopoly on biblical interpretation collapsed within two generations. Scribes — an entire profession — vanished. The Royal Society (1660) and the Académie des Sciences (1666) were invented as institutions specifically to verify claims in the new abundance of printed material. The peer-reviewed journal is a direct response to the printing press.

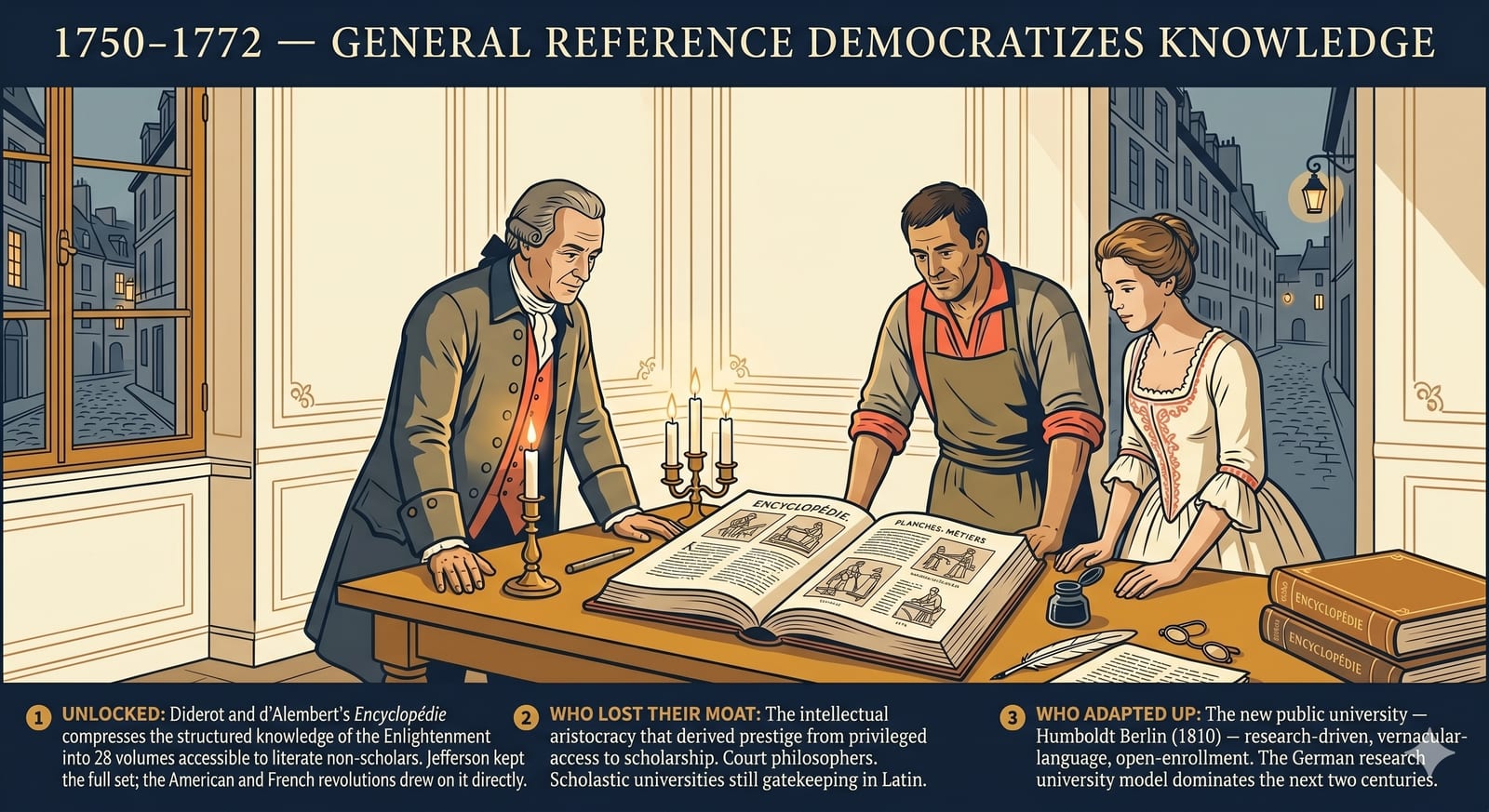

Panel 5 · 1750–1772

The Encyclopédie

Diderot and d'Alembert compressed the structured knowledge of the Enlightenment into 28 volumes accessible to literate non-scholars. Jefferson kept the full set; the American and French revolutions drew on it directly. The Humboldt research university (1810) — research-driven, vernacular-language, open-enrollment — emerged as the institutional response. The German research university model dominated the next two centuries.

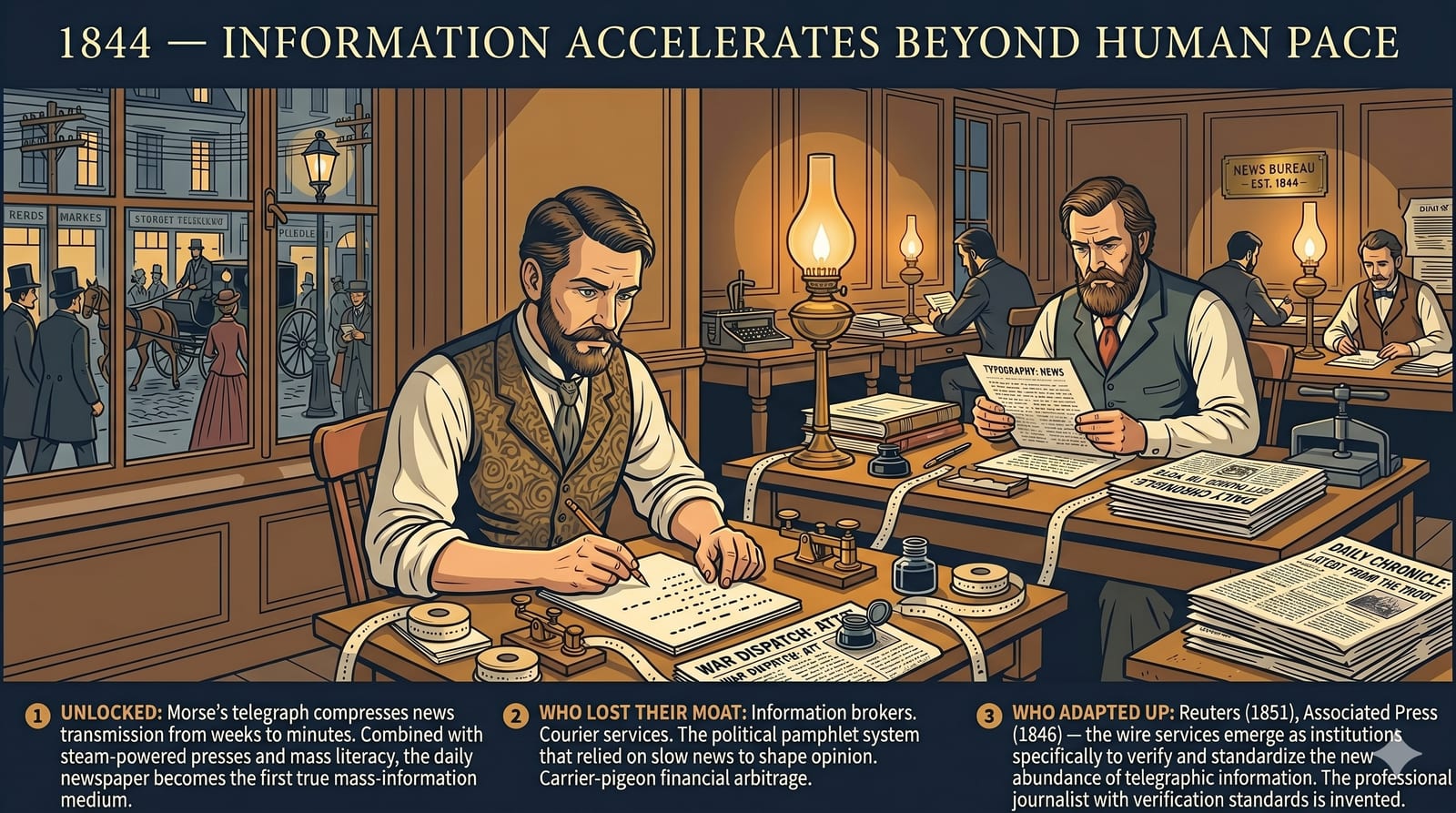

Panel 6 · 1844

Telegraph and wire services

Morse's telegraph compressed news transmission from weeks to minutes. Combined with steam-powered presses and mass literacy, the daily newspaper became the first true mass-information medium. Reuters (1851) and the Associated Press (1846) emerged as institutions specifically to verify and standardize the new abundance of telegraphic information. The professional journalist with verification standards is a direct response to the telegraph.

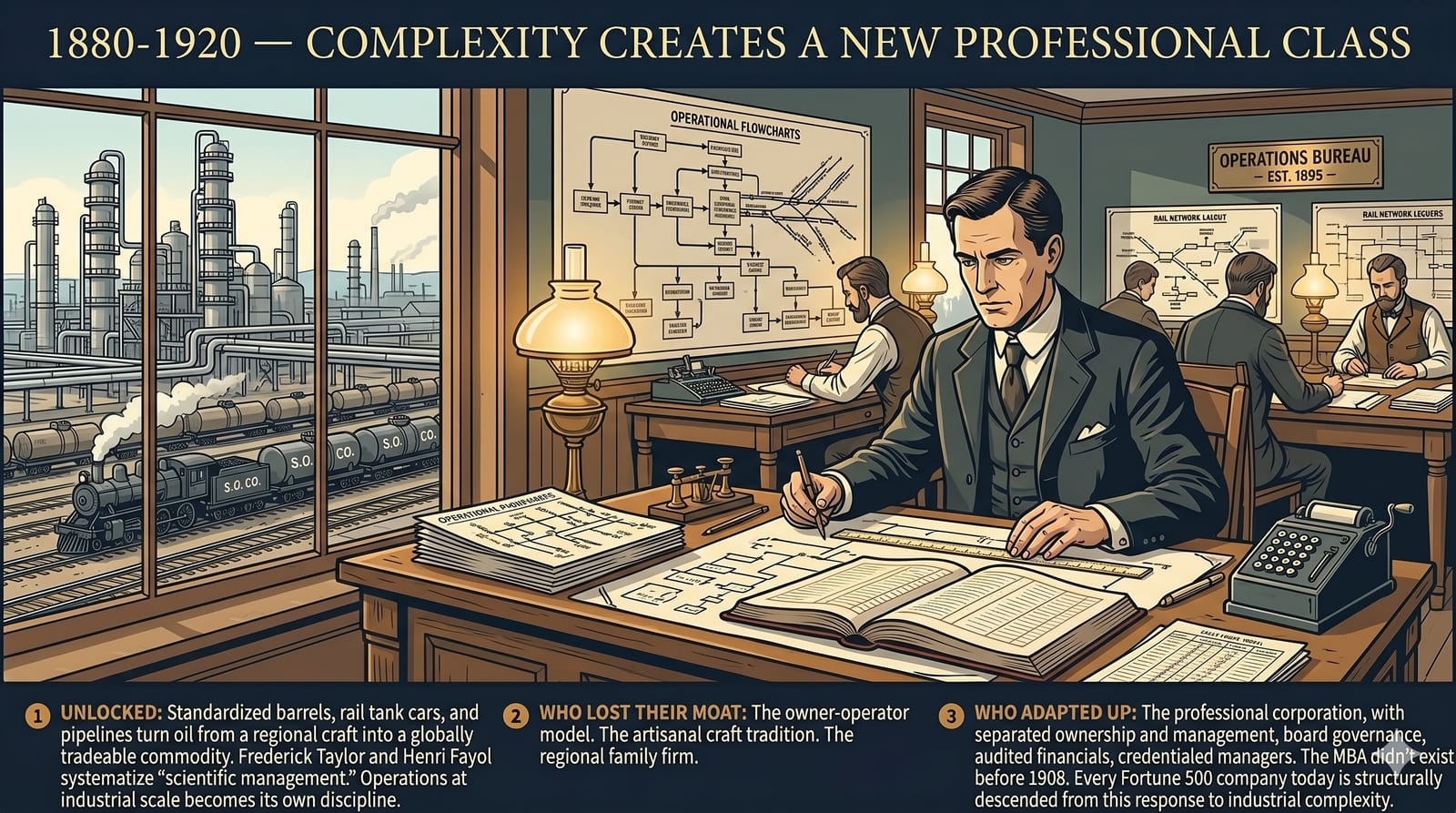

Panel 7 · 1880–1920

Standardized industry and scientific management

Standardized barrels, rail tank cars, and pipelines turned oil from a regional craft into a globally tradeable commodity. Frederick Taylor and Henri Fayol systematized "scientific management." The professional corporation emerged as a new structural form: separated ownership and management, board governance, audited financials, credentialed managers. The MBA didn't exist before 1908. Every Fortune 500 company today is structurally descended from this response to industrial complexity.

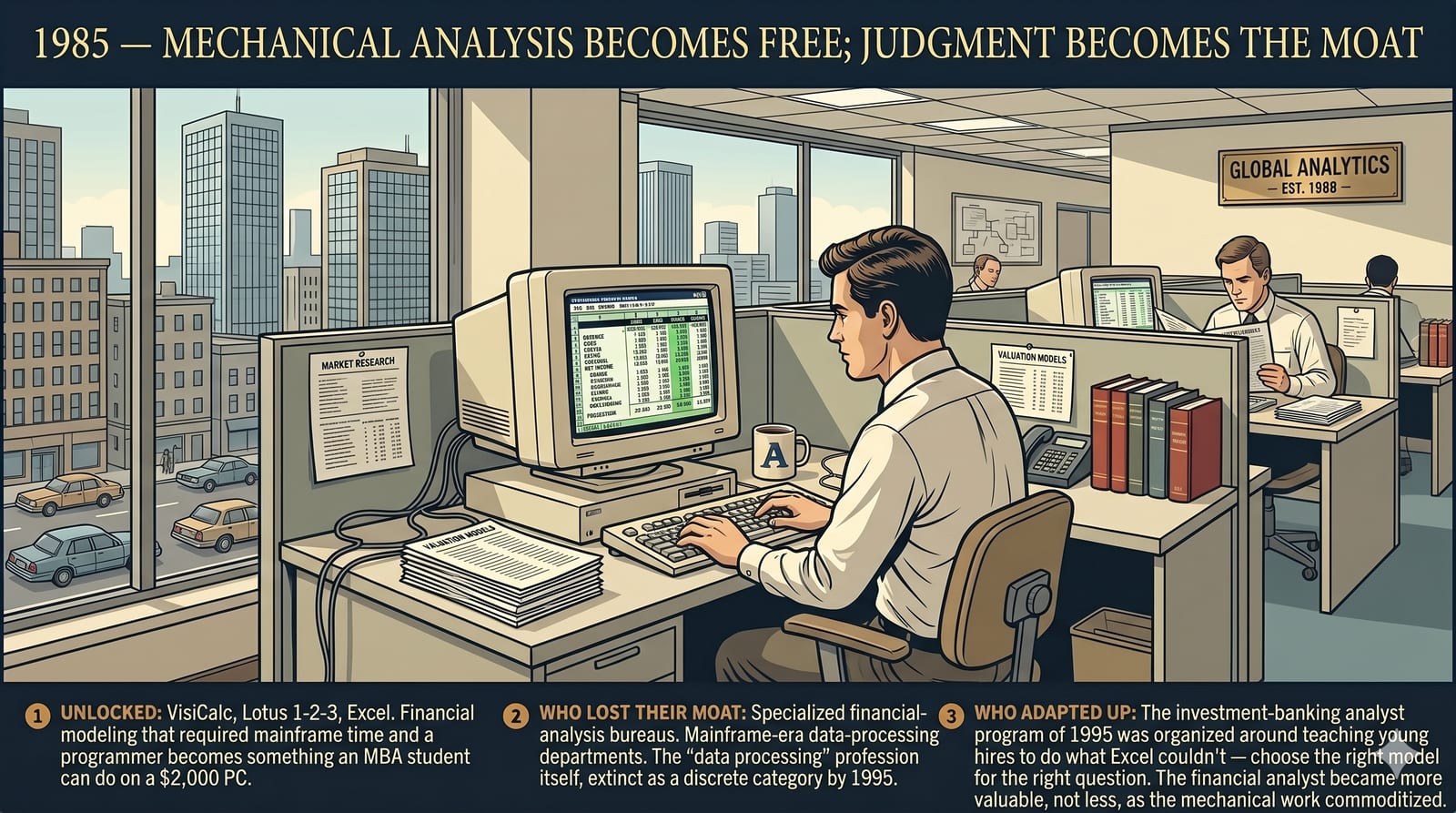

Panel 8 · 1985

Personal computer and Excel

VisiCalc, Lotus 1-2-3, and Excel turned financial modeling that required mainframe time and a programmer into something an MBA student could do on a $2,000 PC. Specialized financial-analysis bureaus and the entire "data processing" profession went extinct as discrete categories by 1995. The investment-banking analyst program of 1995 was reorganized around teaching young hires what Excel couldn't do — choosing the right model for the right question. The financial analyst became more valuable, not less, as the mechanical work commoditized.

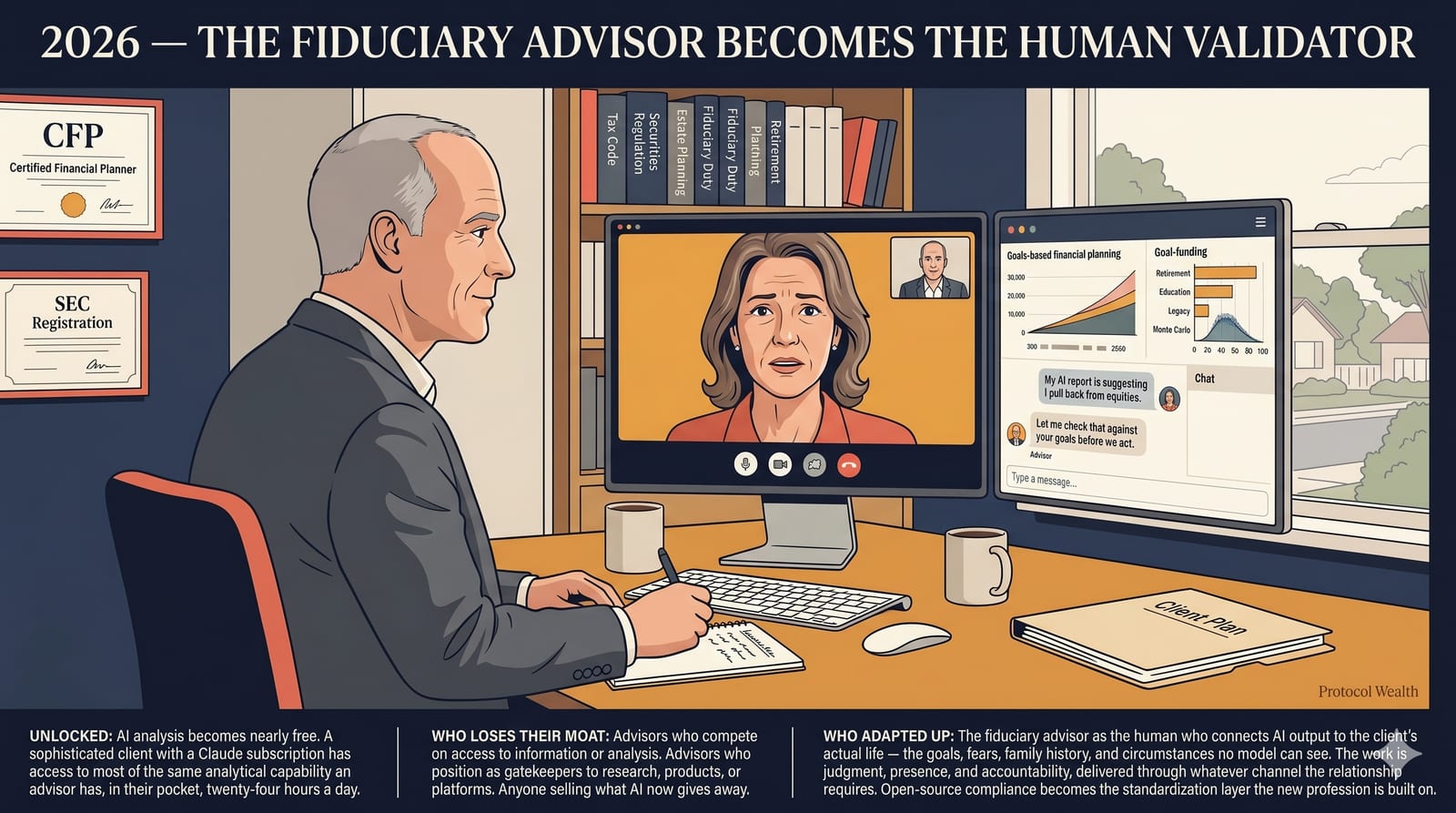

Panel 9 · 2026

AI-augmented fiduciary advice

AI analysis becomes nearly free. A sophisticated client with a Claude subscription has access to most of the same analytical capability an advisor has, in their pocket, twenty-four hours a day. The advisors who lose their moat are the ones who compete on access to information, research, products, or platforms. The advisors who adapt up are the ones who connect AI output to the client's actual life — the goals, fears, family history, and circumstances no model can see. The work is judgment, presence, and accountability. Open-source compliance becomes the standardization layer the new profession is built on.

Section 2

Five convictions

These are positions we operate from, not slogans. Each gets revised when the evidence shifts.

AI commoditizes analysis. Judgment, presence, and accountability become the work.

AI is to financial analysis what Excel was to financial modeling in 1985. Projections, scenario comparison, research synthesis, plan drafting — nearly free. What stays scarce is knowing which question is the right one for this client at this moment, sitting with them when the framework's signal disagrees with their actual situation, and carrying the regulatory accountability that comes with being a fiduciary.

The advisor's role decomposes into three durable functions: validator, accountability holder, behavioral coach. AI supports each; AI replaces none.

Operationally

- We use the Anthropic Citations API for traceable AI output. Native source attribution, preserved through multi-turn reasoning. Building a custom citation pipeline on top of a base model is wasted engineering.

- We self-host Langfuse on our own GCP project for observability. Client data does not leave firm infrastructure for analytics under any circumstance.

- We publish our compliance scaffolding for AI-augmented advice under Apache 2.0. The profession needs shared standards for what auditable practice looks like; firm-specific lock-in is a worse equilibrium for everyone.

Public blockchains become the standardization layer for custody, provenance, and execution.

Custody architecture for digital assets is structurally different from custody architecture for traditional securities. MPC wallets produce a model where the firm has operational signing authority but no unilateral custody; the client retains backup keys, the wallet is structurally non-custodial, and the firm's role is fiduciary oversight rather than asset control. That makes onchain advisory compatible with SEC fiduciary obligations in a way custodial models are not.

The Layer 0 Allocator role — selecting curators, allocating per investment policy, providing fiduciary oversight — is the durable position for SEC-registered RIAs in DeFi vault ecosystems. Layer 2 Curator (RE7, Steakhouse, Gauntlet) is a different role with a different liability surface. We allocate to them. We are not them.

A few specifics

- MPC architecture (Fordefi pattern) with two-of-three signing thresholds. Clients hold backup keys via YubiKey, encrypted recovery phrase, or Coincover.

- Bailment classification of wrapped-BTC strategies has six legal grounds for non-taxable treatment under existing IRS doctrine; Form 8275 disclosure is the right vehicle; shadow-ledger tracking is the operational answer.

- Zero-knowledge proofs become the long-term mechanism for examiner verification without client-data disclosure. Not operational yet. The path is clear, and firms that design for ZK-verifiable compliance now will be the firms whose operations remain examinable as data-disclosure norms shift.

Client data sovereignty is a fiduciary requirement, not a vendor preference.

A fiduciary obligation cannot be honored by a firm that doesn't control where the client's data lives, who can access it, and under what terms it can be used. SaaS vendors change pricing, terms, ownership, and retention policies; a firm whose ability to serve clients depends on a vendor's continued cooperation is structurally subordinated to that vendor.

This is the conviction most likely to make us wrong-looking in the short run. Building firm-controlled infrastructure is operationally harder and slower than buying SaaS. We are choosing the slower path on purpose because the alternative is a fiduciary obligation we don't fully control.

How it shows up

- Anthropic Zero Data Retention is a baseline, not a nice-to-have. Our API access operates under approved ZDR — zero-day input/output retention, US-only inference, no training use. Cloud AI integrations that can't meet this don't touch client data.

- We treat any third-party system of record as transitional. The durable answer is a system of record we build and operate ourselves (PWOS), so the firm's substrate is never hostage to a vendor's roadmap.

The 2025–2045 wealth transfer reshapes how clients evaluate advisors.

There is a conversation we are starting to have more often with the adult children of long-time clients. They are not asking the questions their parents asked. The questions are different in a way that matters, and the difference shows up before the first meeting is even scheduled.

Cerulli puts the number at roughly $84 trillion transferring from Boomers to Gen X and Millennial inheritors over the next two decades. The criteria those inheritors use to evaluate an advisor are not the criteria their parents used. They weight transparency. They weight technology fluency. They weight demonstrated competence over brand and tenure. They read websites carefully. They evaluate published reasoning. They form a view on whether a firm thinks rigorously about what it does before they ever take a meeting.

Open-source publishing is not a marketing flourish — it is a generational trust signal. A younger inheritor reading our public repository perceives transparency in a way a brochure cannot communicate. The signal is the substance.

Three wealth situations carry the most leverage in this transition, and they are the situations traditional advisory models are not structured to serve well. Concentrated equity in a single name. Token wealth held by founders or early employees. Protocol treasuries managed by DAOs and foundations. Each one breaks the assumptions that drive standard wealth-management pricing — that the assets are liquid, that they fit a 60/40 mental model, that an AUM fee meaningfully aligns incentives. Charging a percentage of AUM on an illiquid concentrated position is not aligned compensation — it is a fee that grows when the client's risk grows, on assets the client cannot easily sell. Fee-for-service is the right structure for wealth that is illiquid or pre-liquidity, and it is the structure we use.

The profession is in a sorting event. Not all firms make the transition.

We have been in this profession long enough to recognize what a sorting event looks like. The last one ran from roughly 1985 to 1995, when VisiCalc and Lotus and Excel turned financial modeling from a mainframe-and-programmer task into something an MBA student could do on a $2,000 PC. The analysts who adapted up — who learned to choose the right model for the right question — became more valuable, not less. The data-processing bureaus that competed on access to compute went away.

The current sorting event is structurally identical, and it is not a prediction. It is observable now, in the firms we share clients with. Some firms are adapting up. They are integrating AI into the research and planning workflow. They are publishing their reasoning. They are investing in technology fluency. They are taking fiduciary accountability seriously enough to build the infrastructure that accountability requires. Other firms are not. They are continuing to compete on relationships and brand. They are treating AI as a content tool. They are gradually losing ground without quite naming what is happening.

Two consequences worth naming, because both will surprise the consultants modeling the industry from the outside.

The first consequence is that the "channel" framing in industry analysis is becoming obsolete. Wirehouse, IBD, RIA, hybrid — those labels are about how a firm is structured, not about what kind of firm it is. The relevant axis going forward is not the channel. It is whether a firm is technology-native and fiduciary-fluent, or whether it is neither. We expect the T3-style category surveys that the profession reads to follow this shift, but on a multi-year lag. Industry analysis is a trailing indicator.

The second consequence is that the distribution of advisory firms ten years from now will be bimodal — not normal. Sophisticated, transparent, fiduciary firms with technology-native infrastructure at one pole. Self-directed clients using AI for routine work at the other. The continuum of mid-tier traditional practices in between thins substantially. The middle is where most of the profession lives today, and it is where the sorting event will be felt the hardest. Firms that recognize the bimodal early have time to position. The firms that recognize it late do not get the time back.

Section 3

What we expect to be wrong about

The biggest gap: we don't know how compressed the timeline is. The Excel transition for analysts ran roughly a decade. The AI transition could run three years or fifteen, and the operational decisions we make today (build PWOS, self-host observability, control our own compliance infrastructure) all have payback periods that assume the longer end. If the compression is closer to three years, some of these investments are over-engineered relative to the window. We accept that risk because the alternative — buying SaaS and hoping the vendor's terms align with our fiduciary obligation indefinitely — is the worse failure mode.

We also don't know whether the verification layer we describe is a stable equilibrium or a transitional phase. Every prior layer shift produced a durable verifier role; this one might not, because the verifier itself can be partially automated in a way the printing press never threatened the editor. We hold the position because the historical pattern is the best base rate available, not because we think it's certain.

We will mark the change history when our reading shifts.

References

We synthesized this argument; we didn't invent it. The layer-shift framing builds on work by thinkers who articulated the structural dynamics before us.

- Joel Spolsky, "Strategy Letter V," Joel on Software, 2002. When one layer of a stack commoditizes, value migrates to the adjacent layer.

- Clayton Christensen and Michael Raynor, The Innovator's Solution (Harvard Business School Press, 2003). The Law of Conservation of Attractive Profits.

- Marc Andreessen, "Why Software Is Eating the World," The Wall Street Journal, August 20, 2011.

- Carlota Perez, Technological Revolutions and Financial Capital (Edward Elgar, 2002). Installation and deployment phases of technological revolutions.

- Clay Shirky, Here Comes Everybody (Penguin Press, 2008). Institutions under information abundance.

- Mark Lemley and Brett Frischmann, "Scarcity, Regulation, and the Abundance Society," 2022. How legal and economic institutions adapt when previously scarce resources become abundant.

- César Hidalgo, Why Information Grows (Basic Books, 2015). Knowledge as crystallized information that accumulates in people, products, and networks.

- George Akerlof, "The Market for 'Lemons,'" Quarterly Journal of Economics 84, no. 3 (1970). When barriers to entry drop and quality becomes hard to distinguish, demand for verification and certification emerges.

- Bob Veres, Inside Information. The advisory profession's center of gravity shifting from access to verification.

Section 4

Change log

Reframed thesis around layer shifts and the emerging verification layer. Consolidated lineage into inline citations with compact reference list. Removed vendor-specific operational detail from convictions.

Initial publication. Five convictions, supporting positions, lineage, gaps.

Last updated: July 27, 2026. Protocol Wealth LLC is an SEC-registered investment adviser (CRD #335298). See ourForm ADVfor authoritative regulatory disclosures.

Registration with the SEC does not imply a certain level of skill or training. Advisory services are provided only under a signed advisory agreement. This page describes the firm's operating thesis and is not a solicitation, recommendation, or guarantee of results.

All investments involve risk, including the potential loss of principal. Past performance does not guarantee future results.